Long: United Rentals Inc. (NYSE: URI) (5/28/2024)

Write-Up on United Rentals

Charlie Martin

28 May 2024

Long: United Rentals, Inc. (NYSE: URI)

Business Overview:

United Rentals (NYSE: URI) is the largest industrial rental company in the world, with 1,520 North American locations and 80 international locations, mostly in New Zealand and Australia, totaling 1,600 global locations. United Rentals has a fleet of over 1 million pieces of equipment, broken down into 4,800 equipment categories, and a fleet value of $20.66 billion. United Rentals breaks down their business into two categories: General Rentals and Specialty Rentals. General Rentals include equipment such as bulldozers, trucks, excavators, etc and Specialty Rentals include equipment such as fluid solutions, power & HVAC, trench safety, etc.

United Rentals business model goes as follows: they purchase equipment from OEMs (original equipment manufacturers), they then rent out that equipment to construction companies, infrastructure companies, industrial companies, etc over a 5-7 year period (depreciating it on the balance sheet over those years), and then they sell that used equipment in the secondary market. Some equipment they use for longer periods before selling in the secondary equipment, could be up to a 40 year period, and some equipment they sell in a shorter time frame.

Their main competitors are Ashtead Group plc and Herc Holdings. Ashtead is the parent company of Sunbelt Rentals and currently has 11% of U.S. market share and Herc has 4% of U.S market share. United Rentals has the largest share of the U.S. rental market with 15%. Their main customers are “Industrial & Other” at 49%, “Non-residential construction” at 46%, and “Residential construction” at 5%.

Investment Thesis:

United Rentals is an attractive business and a Buy at $665.12/share because of the secular growth trend of the rental business, their strategic M&A in a fragmented market and smart capital allocation, the scale advantages they have from being the largest rental business, their focus on specialty rentals, high dollar utilization, and low valuation. I believe that all of these factors give United Rentals a long-term competitive advantage over their competitors (Ashtead and Herc) and will contribute to long-term earnings growth, margin growth, and stock price growth. At the end of this write-up are 3 different discounted cash flow models—one with the worst case scenario, one with the scenario the market believes will happen, and one with the scenario I believe is most likely.

Analysts have pointed out some potential headwinds to United Rentals including cyclicality, competition from OEMs, high balance sheet leverage and capital intensive business model, however, I don’t believe these pose as significant of risks as the market believes.

Secular Growth of the Rentals Business

Industrial manufacturers and companies (which includes everything from construction companies to mining companies) have transitioned away from owning their own equipment to renting equipment from companies like United Rentals. In 2023, rental penetration was 55% for general tools, which is up from 10% in 1990 and 25% in 2000. This, however, is still considerably lower than rental penetration in Japan, UK, and Europe more broadly, which sit at 80%, 80%, and 65%, respectively. Over the coming years and decades, U.S rental penetration will likely trend upwards, with United Rentals poised to capture this upwards trend. Overall, the U.S. industrial rental market has grown at a 5.2% CAGR over the past 25 years.

Industrial manufacturers and companies have chosen to systematically transition away from buying and towards renting for a few reasons. In the case of highly capital intensive equipment, such as bulldozers, forklifts, trucks, etc, renting the equipment reduces their balance sheet risk and lowers the barrier-to-entry in order to take on a project or start a business. Instead of having to buy many bulldozers, which would likely cost millions, companies can rent the bulldozers only when they need them, removing that capital risk off of their balance sheet. By renting from United Rentals, companies outsource maintenance, warehousing, equipment failure risk, etc.

With specialty solutions, such as trench safety equipment, chemical treatment equipment, or specialized repair equipment, renting is an attractive option because they may only need to use that equipment once, as it costs the renter less in the long-run. United Rentals, however, can use this specialized equipment many times with different customers over its life-cycle. As I will talk about later, specialty rentals are an attractive growth area for United Rentals because Specialty Rental penetration is only ~20-25% and has higher gross margins than General Rentals. United Rentals’ Specialty business has grown at a 24.2% 10-year CAGR.

Other reasons that companies have chosen to rent are reliability and quality of the equipment, customer support and service, managing OSHA risk, reducing downtime, focusing on core business, and more.

Fragmented Market, Strategic M&A, and Smart Capital Allocation

Although United Rentals is the largest U.S. rentals business, there are a lot of future growth opportunities because of the fragmented nature of the rentals market. As of the end of 2023, United Rentals, Ashtead, and Herc only accounted for 30% of the rentals market, and 60% of the rentals market is made up of rentals companies outside the top 10 rental companies. United Rentals has catapulted itself to its industry leading position through acquisitions, acquiring over 300 companies since its inception. In 2010, United Rentals only commanded 5% of market share compared to 17% today. In recent years, United Rentals has slowed down the pace of its acquisitions, choosing to be more strategic about the markets it chooses to enter and the price it is willing to pay.

To highlight this, let's look at their most recent acquisition, Yak Access or Yak Mat. Yak is the industry leader in hardwood, softwood, and composite mats in the U.S. United Rentals completed its acquisition of Yak Mat on March 15, 2024, paying $1.1 billion in cash or 6.4x LTM EV/EBITDA. This acquisition is demonstrative of United Rentals’ transition into specialty markets, which tend to have much higher EBITDA margins (in this case 48% EBITDA margins), less competition, and larger growth runways. United Rentals is also quick to take advantage of synergies and cross selling with acquisitions, as in the 2 months they have owned Yak Mat, they have capitalized on $7 million in cost synergies. Acquiring at 6.4x EV/EBITDA implies a 15.6% estimated return and factoring the cost synergies, the EV/EBITDA is 6.17x, which implies a 16.2% estimated return on the investment.

The second acquisition that I think is important to talk about is their 2012 acquisition of RSC, which was at that point the 3rd largest rental company in the United States. Through acquiring RSC, United Rentals gained the clear #1 spot in the rental industry, where the advantages of scale are massive. While United Rentals did pay a premium at 8.4x EV/EBITDA, the synergies and cross-selling totaled roughly $250 million, which made the post-acquisition valuation much more attractive at 5.3x EV/EBITDA. This implies a post synergies and cross-selling return of 19.2%. The advantages of scale, which I will talk about later in this write-up, are compounding, and accretive to margin growth, time utilization growth, and revenue growth.

As far as capital allocation goes, United Rentals historically spends ~⅔ of total capital deployed on CapEx, which is mostly new equipment, and ~⅓ on acquisitions, and modulates those numbers downwards during worse financial markets or upwards during better financial markets. United Rentals’ ROIC is low at 13.6%, but it is slightly higher than Ashtead’s ROIC of 12.65%, which indicates that the low ROIC’s are more of a industry-wide issue, rather than a United Rentals specific issue. United Rentals’ ROIC has also gone up significantly in the past two years, from 10.9% in 2022 to 13.6% in 2024. United Rentals has also sizeably lowered their leverage ratio in the past 10 years, from 3.6x to 1.7x, meaning that they are both more financially stable and could possibly take on more debt if they wanted to do acquisitions. Finally, United Rentals has a ~1% yielding dividend per year and is buying back ~$1.5 billion in stock over the next year, showing their commitment to returning shareholders value.

Scale Advantages

As the largest equipment rental company, United Rentals enjoys many scale advantages, with the first being pricing power. Because United Rentals is the biggest buyer from many of their OEMs, they are consistently able to get a 25-30% discount on equipment. This gives them a competitive advantage over many smaller rental companies who don’t have the order size to have that kind of bargaining power, but this power isn’t quite as translatable to bigger competitors, such as Ashtead, who also have significant bargaining power. Through acquiring small rentals companies, United Rentals will be able to use their bargaining power to instantly increase bottom line margins.

United Rentals’ scale at 1,600 global locations allows them to take advantage of equipment sharing, where they have the requisite density of locations to be able to share 1 piece of equipment across many different locations. By doing this, United Rentals can increase their time utilization (the % of time that a particular piece of equipment is being used), their dollar utilization (the amount of rentals dollars that a piece of equipment generates compared to the total value of the piece of equipment), and thus their bottom line margins and profit. This effect only increases as they have more locations in a certain area, and it makes their unit economics far more attractive than small scale rentals businesses. Again, with acquisitions, United Rentals will integrate smaller rentals businesses into their equipment sharing network, which would be margin accretive to the acquired business.

With over 4,800 equipment rental units, United Rentals can take advantage of cross sellings, where they are the one-stop-shop provider for a project. For example, on a construction site, not only can they provide forklifts, bulldozers, power tools, and those items, United Rentals can also provide the plastic bathroom facilities, storage, fans, etc. A construction site would thus be more likely to rent from United Rentals for everything, instead of a different rental company for each piece of equipment on their site, as the uniformity makes it more efficient and less expensive. This horizontal integration is a key part of United Rentals’ future acquisition strategy.

Focus on Specialty Rentals

United Rentals’ focus on specialty rentals as an area for growth will be margin accretive and offer new avenues for long term revenue growth. Specialty rentals, which United Rentals lists as Fluid solutions, Power & HVAC, Reliable Onsite Services, Trench Safety, etc, are a considerably smaller market than general rentals. United Rentals have focused on specialty rentals as a growth area over the past 10 years, with a 24.2% revenue CAGR over the past 10 years. In 2013, specialty revenue only accounted for 9.5% of their total revenue compared to 28.8% in 2023. Compared to general rentals, which have a 60/40 rent/own rate, specialty rentals only have a 20/80 rent/own rate. This means that even though they have experienced a lot of growth in their specialty revenue segment, there is still a lot of room for growth, as there is no reason that specialty rental own/rent rates wouldn’t trend towards that of general rentals.

Specialty rentals also have better unit economics than general rentals, driven by higher time utilization, scarcity of that specific piece of rental equipment, and pricing power. Because of the scarcity of specialty equipment for rent, there is a larger amount of demand per piece of equipment than general rentals. This scarcity feeds into pricing power, as there is a less saturated competitive landscape. Finally, specialty rentals tend to have less cyclicality than general rentals. All of these factors add up to make specialty rentals have considerably higher gross margins than general rentals (48.9% gross margins for specialty in 2023 vs 36.6% gross margins for general rentals in 2023). As specialty revenues become a larger part of United Rentals’ total revenue, their overall gross margins will increase.

United Rentals’ acquisition strategy has been focused on further increasing specialty rentals, evidenced by their acquisition of Yak Mat, General Finance Corp, and BakerCorp.

It should be noted that Ashtead is also focusing on increasing their specialty revenues, but I don’t think it is necessarily a zero-sum game. However, I think United Rentals has a slight competitive advantage over Ashtead because of their scale, capital for acquisitions, and existing specialty infrastructure. Currently, 38% of United Rentals’ locations are specialty rentals locations, and as that number gets larger, they can further take advantage of equipment sharing.

Dollar Utilization

Dollar utilization is the key performance metric for a rentals business. What dollar utilization represents is how much rental revenue a company can generate per year as compared to the OEC (original equipment cost). For the trailing 12 months, United Rentals generated $12.253 billion in equipment rental revenue on $20.66 billion of original equipment cost, implying a dollar utilization rate of 59.3%.

Let’s look at how this plays out with an example. On year 1, United Rentals purchases a piece of equipment from an OEM for $100. United Rentals then generates $59.3 dollars of revenue on that piece of equipment in years 1-6 (for our example). Over that 6 year period, United Rentals will generate ~$360 of revenue on a $100 piece of equipment. At year 6, United Rentals goes to sell that piece of equipment, where resale values are typically between 54%-63% of the price of the original value of the equipment. For this example, let's use 58%, which means they are able to sell that piece of equipment for $58 dollars. In total, over the life cycle of a piece of equipment, they are able to generate $418 dollars of revenue on $100 of OEC.

This is almost identical to Ashtead’s normalized dollar utilization of 59.6% over Canada, UK, and the U.S. While United Rentals’ dollar utilization level isn’t a competitive advantage for them right now, their dollar utilization level will only increase as they have a greater density of locations, greater proportion of specialty rental revenue, and reach a larger scale.

Valuation

At the end of this write-up, I attached 3 different discounted cash flow models that I constructed myself. The first assumes the worst case scenario, which I believe to have a <5% likelihood of happening. In that model, the fair value per share is $483.56.

The next discounted cash flow model is what I believe the market currently sees as the valuation for United Rentals. I tried to use analyst estimates for revenue growth and EBIT margins, as well as the market calculated WACC, to backtrack into what the stock price is currently trading at. I believe this case has a ~30-40% chance of happening. The fair value per share in that case is $688.19.

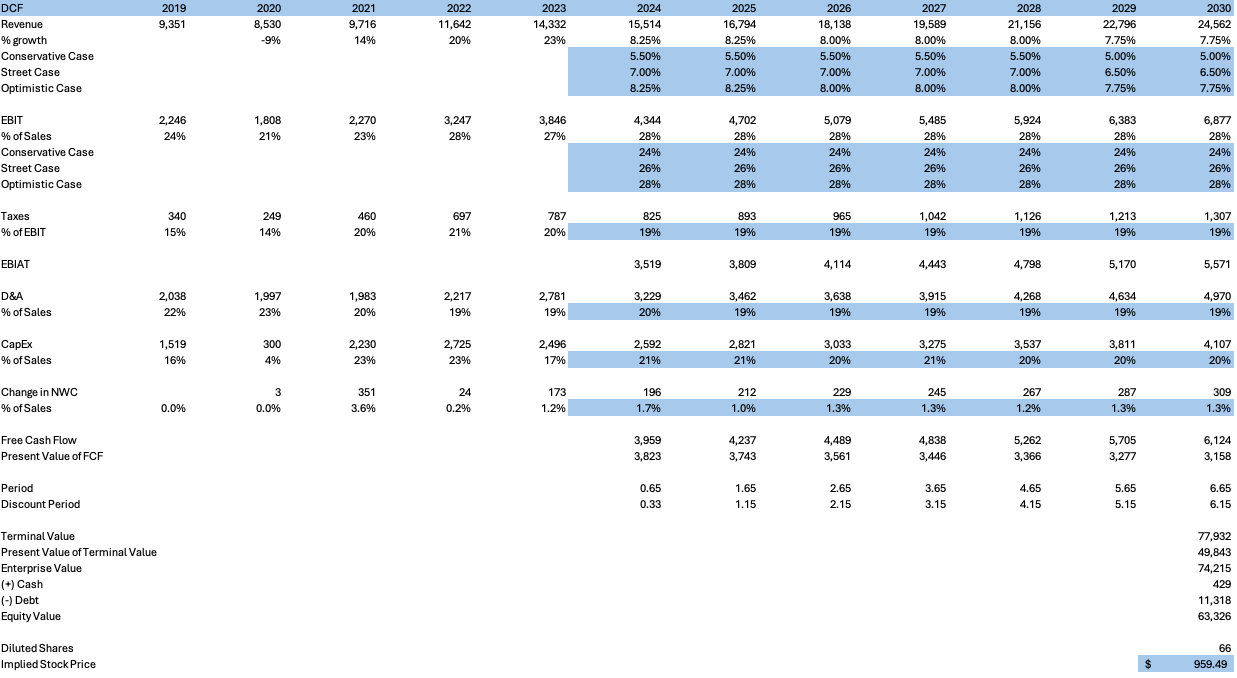

The final discounted cash flow model is what I project happening for United Rentals. Most notably, I believe that revenue growth will be on average 300 bps higher than what the market currently believes because of specialty rental growth and smart M&A and that EBIT margins will be 200 bps higher than what the market currently believes because of scale advantages and margin accretive specialty rental revenue growth. Finally, I believe that the discount rate for United Rentals is artificially high because of its beta (1.51 unlevered and 1.82 levered, I used unlevered because I don’t plan on using leverage). For my assumption, I adjusted the WACC down by 100 bps. I think there is a ~55%-65% chance of this scenario occurring. With this set of assumptions, the fair value per share is $959.49, representing a 44% margin of safety or potential upside to the fair value per share.

In the footnotes of the models, I will attach all assumptions that I used when building them. If you would like to play around with the interactive and dynamic model, email me at charlie.martin@yale.edu, and I will forward the Excel file to you.

As far as traditional valuation multiples go, United Rentals trades a 8.56x LTM EV/EBITDA, 18.28x LTM P/E, and 5.2% LTM unlevered free cash flow yield. This is slightly lower than Ashtead, which trades at 8.88x LTM EV/EBITDA, 19.68x LTM P/E, and a 4.17% LTM unlevered free cash flow yield.

Risks

Cyclicality

At face value, United Rentals seems like a cyclical business; that logic is relatively simple, and goes as follows: poor economy=less spend on construction and infrastructure=less money spent on construction rentals. However, this is only first-rate logic. This is, in some senses, counterbalanced by a sense of countercyclicality. That logic goes: poor economy=less spend for construction and infrastructure companies=companies are more likely to rent their equipment. versus buy their equipment. While this might not fully balance out the effects of a poor economy, it provides some semblance of a counterweight.

In poor economic conditions, United Rentals decreases their spend on new equipment, which increases their free cash flow, making their balance sheet more protected to harsh economic conditions.

Competition from OEMs

Caterpillar has recently gotten into the rentals game, beta testing this strategy in the Chicago area. Given the success of rentals businesses, Caterpillar sees that they can slightly undercut the prices of United Rentals and Ashtead because they are the manufacturer of the equipment. I don’t see this strategy working at all. First, caterpillar has an extremely limited fleet of equipment as compared to rental companies, meaning that they can’t possibly be a one-stop-shop for construction sites. Second, even though they could in theory charge lower prices, they lack the distribution network that rentals companies. As I have laid out in this write-up, scale and distribution networks are essential to United Rentals’ success—OEMs don’t have any customer-facing distribution networks, and the investment that they would need to make to build this distribution network would be very large. Finally, for OEMs to seriously compete with rentals companies would take complete shareholder, board, and executive alignment, which I don’t think is likely in these highly mature businesses where large and spontaneous CapEx spend is frowned upon.

Leverage Ratio and Capital Intensive Business Model

One of the biggest gripes that investors and analysts alike have concerning United Rentals, and rentals businesses writ large, is the high leverage ratio that this business requires. It is inherently capital intensive to purchase vast swaths of equipment, but United Rentals has increasingly used their cash flow to finance these purchases, decreasing their overall leverage ratio. Over the past 12 years, United Rentals has made a concerted effort to lower their leverage ratio, going from 3.6x to 1.7x. United Rentals has also proved the durability of this leverage during financial crises, with seemingly no issues during the COVID-19 drawdown in 2020 and the interest rate increases in 2022 and 2023.

Conclusion

If you got this far, thanks so much for reading. Please direct any questions to the comment section on my Substack (https://charliemartin.substack.com/) or to my email (charlie.martin@yale.edu). I wanted to give a thanks to the Substacks of Analyzing Good Businesses and TQI Capital for helping orient me to the key drivers for this business. I got some inspiration from these two write-ups. The models are right down below this, as well as the WACC calculation. This isn't investment advice or solicitation, use for purely informational and educational purposes, and please do your own diligence. Thanks again, for reading! <3

Worst Case Scenario for URI (2024 Rev Growth of 5.50%, EBIT margins of 24%, WACC of 13.36%, TGR of 2.25%)

Street Case for URI (2024 Rev Growth of 7%, EBIT margins of 26%, WACC of 12.36%, TGR of 2.75%)

My Personal Prediction for URI (2024 Rev growth of 8.25%, EBIT margins of 28%, WACC of 11.36%, TGR of 3.25%)

WACC